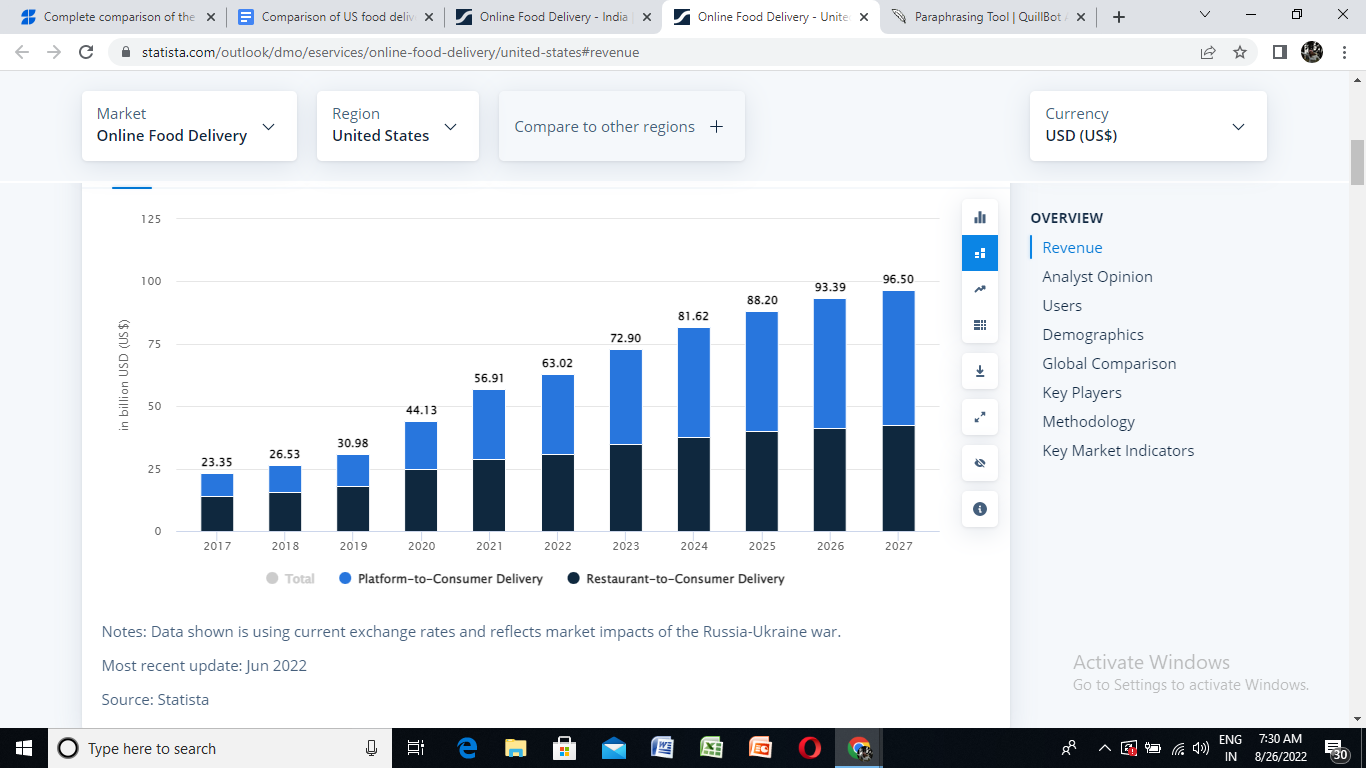

The United States is regarded as an international leader for various reasons. One of these is the developments in technology they bring about. They set the pattern almost all of the time, and the rest of the world follows. A similar situation has occurred in relation to cell phones and the most popular on-demand food delivery services in the USA for 2022–2023. They established the fad. The size of the US food delivery business is anticipated to reach $40 billion by 2023, while India’s market is anticipated to be $5 billion.

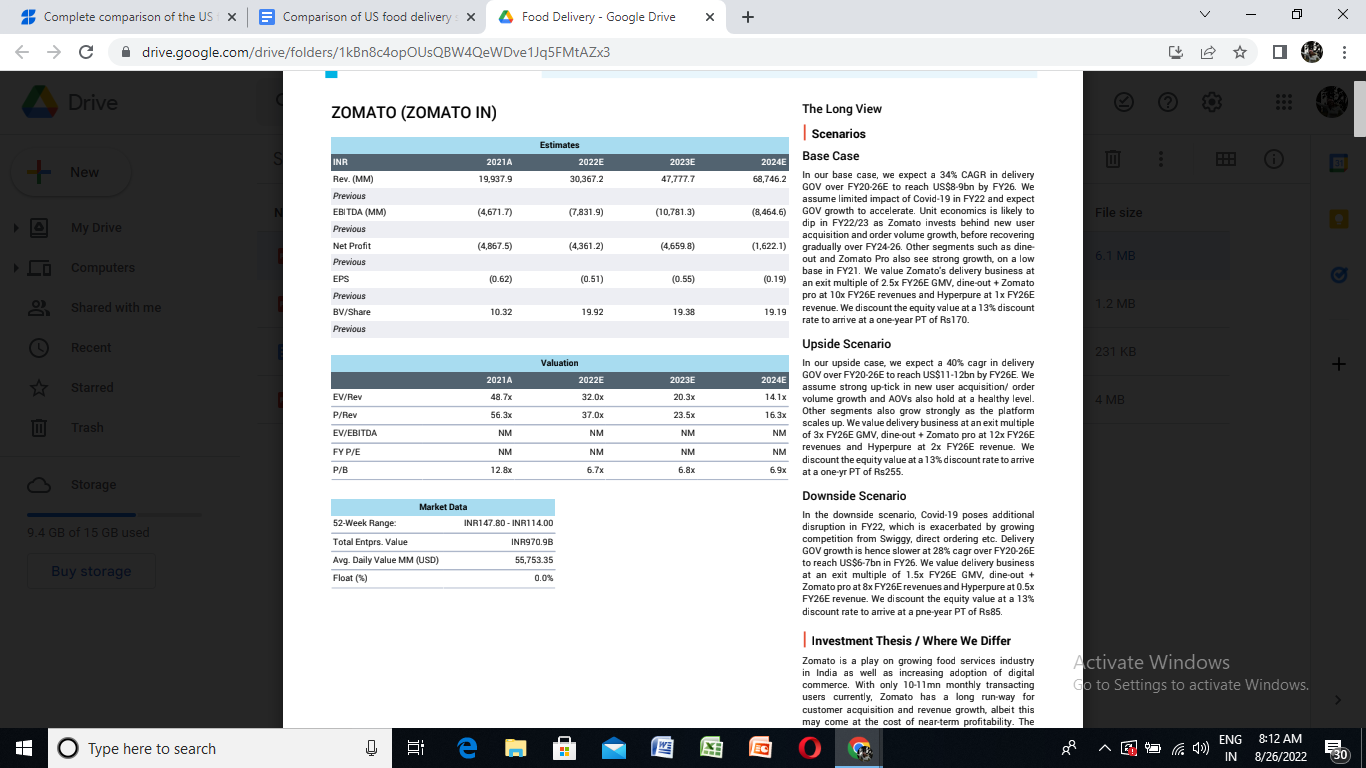

Revenue of Indian delivery app stocks:

Revenue of US delivery app stocks:

US food delivery landscape vs Indian landscape

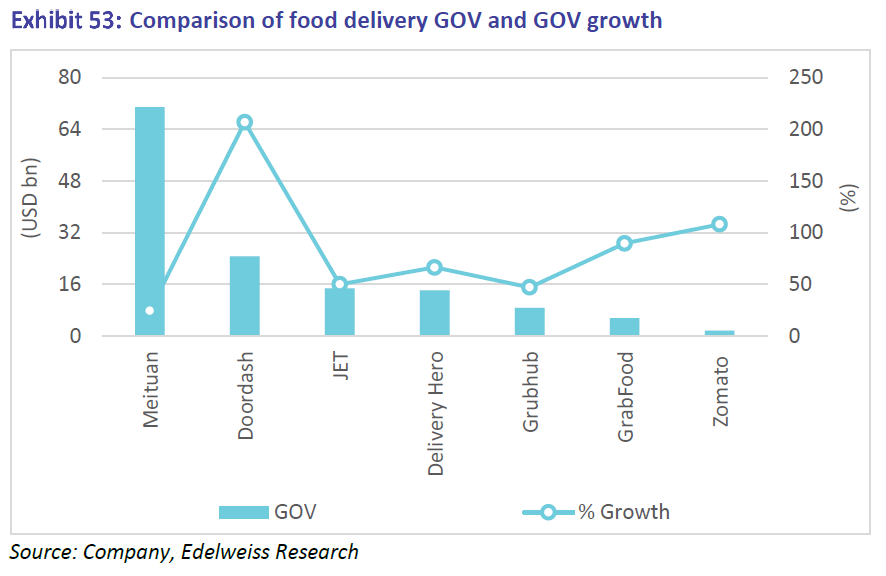

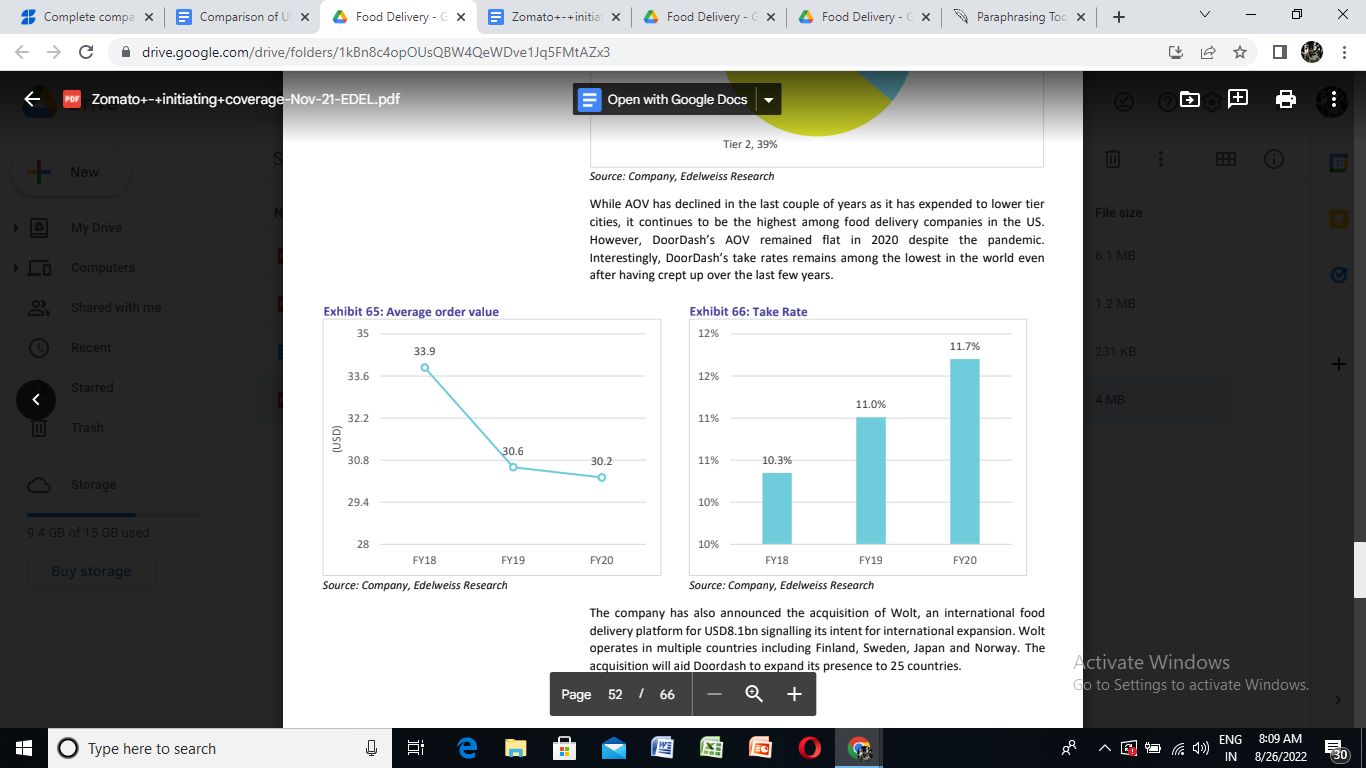

While the US is expected to have a food delivery platform penetration of up to 20% by 2021, India’s was only approximately 4% overall and 33% in the top 20 cities during the same period, despite India’s significantly greater internet and smartphone participation of 690 million users in CY20. Compared to 38% in the United States and 53% in China, only 10% of Indians have regular access to online meal delivery. Additionally, below 10% of Indians’ total meal expenditures are made at restaurants, compared to between 40 and 50 percent in the US and China. Additionally, Meiutan, the biggest food delivery service in the world, sends out 850 million packages in one month (65 percent of the market). Nearly 70 million orders are fulfilled each month by the biggest corporation in the US (55% market share).

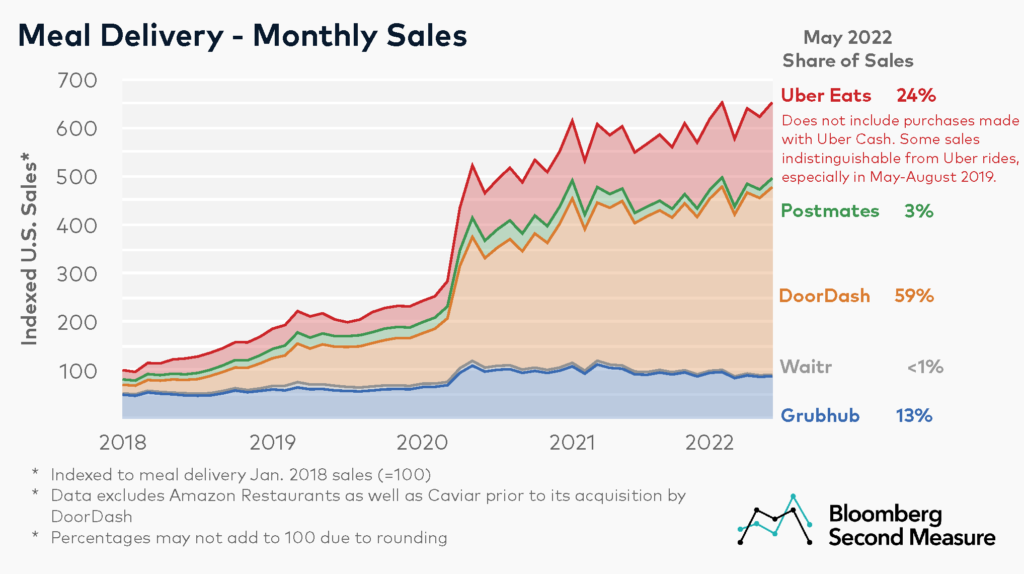

DoorDash is dominating the US markets

DoorDash (DASH), one of the largest US delivery app stocks with over 57% market share in the U.S. as against 18% in 2018, operates in around 4,000 cities and has over 340,000 stores in the U.S and Canada. It coordinates the activities of all three segments involved along the delivery chain: Restaurants, Delivery Agents (Dashers) and Customers and by far the largest third-party delivery service in the U.S.

Customers can order from a whole host of menus from the comfort of their homes, and restaurants can expand their online presence and serve a larger market without hiring their own delivery agents. Dashers provide real-time location updates to customers and receive a flat amount per weekly delivery. Today, the platform boasts over 20 million active consumers and processed $9.9 billion in Gross Order Value (GOV) in Q1 2021. The company currently has about 20 million Monthly Active Users (MAUs), and the total number of orders grew over 3x in 2020 to 816 million.

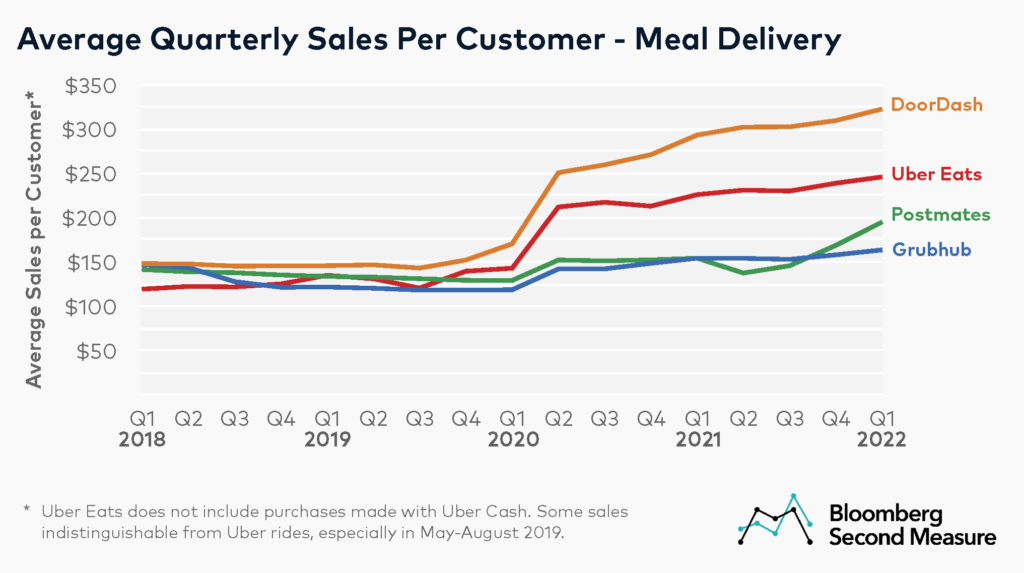

Along with more customers using meal delivery services, these businesses’ average sales per client have increased throughout the epidemic. Over the previous two years, average sales per client have increased the most on DoorDash stocks and Ubereats stocks. The average revenues per customer in DoorDash stocks increased by 89 percent during the first quarter of 2022 compared to the same period in 2020. Uber Eats’ average sales per client in the same period increased by 72%. Customers of DoorDash spent the most, on average $323 each, during the first quarter of 2022. The average quarterly customer spending at UberEats was $246, whereas the average quarterly customer spending at Grubhub and Postmates was $163 and $195, respectively. As food and petrol prices rise, consumers may soon be forced to pay a higher price for meal delivery services. Different meal delivery services have reacted to these inflationary pressures. For instance, in March 2022, Uber Eats started charging customers a gasoline cost. To help drivers cope with rising fuel prices, DoorDash introduced a petrol rewards program, whilst Grubhub increased driver compensation per mile.

Subscriptions are a newly developing solution as food delivery firms explore new strategies to expand in major and small locations. In 2016, Postmates introduced Postmates Unlimited, and in 2018 and 2020, DoorDash stocks and Grubhub stocks did the same with their membership services. Uber also debuted its brand-new “Uber One” subscription package in November 2021, which provides advantages for both rides and delivery services. 30 percent of DoorDash’s clients in May 2022 were DashPass subscribers. An average of 69 percent of cohorts subscribed with DashPass between May 2021 and May 2022 continued to be subscribers after one month. DashPass has an average customer retention rate of 42% over six months and 32% for twelve months. DoorDash also introduced DashPass for Students in April 2022, which provides the advantages of the subscription at a lower cost.

GrubHub Stocks

Several deliveries made during the pandemic were powered by Grubhub (GRUB), another food delivery business with relationships with eateries, which also experienced an increase in sales. According to NASDAQ, eager investors drove the share prices higher, up, and away when the meal delivery network went public in 2014. According to BNN, pandemic-related lockdowns have made the food delivery business a true money-printing machine by the middle of 2020. Therefore, in a rather predicted move, the nearly unanimous majority of Grubhub stocks holders approved the company’s acquisition by Just Eat Takeaway for the large sum amounting to $7.3 billion (via CNBC). As a result, stockholders in Grubhub became owners of this huge parent company.

UberEats Stocks

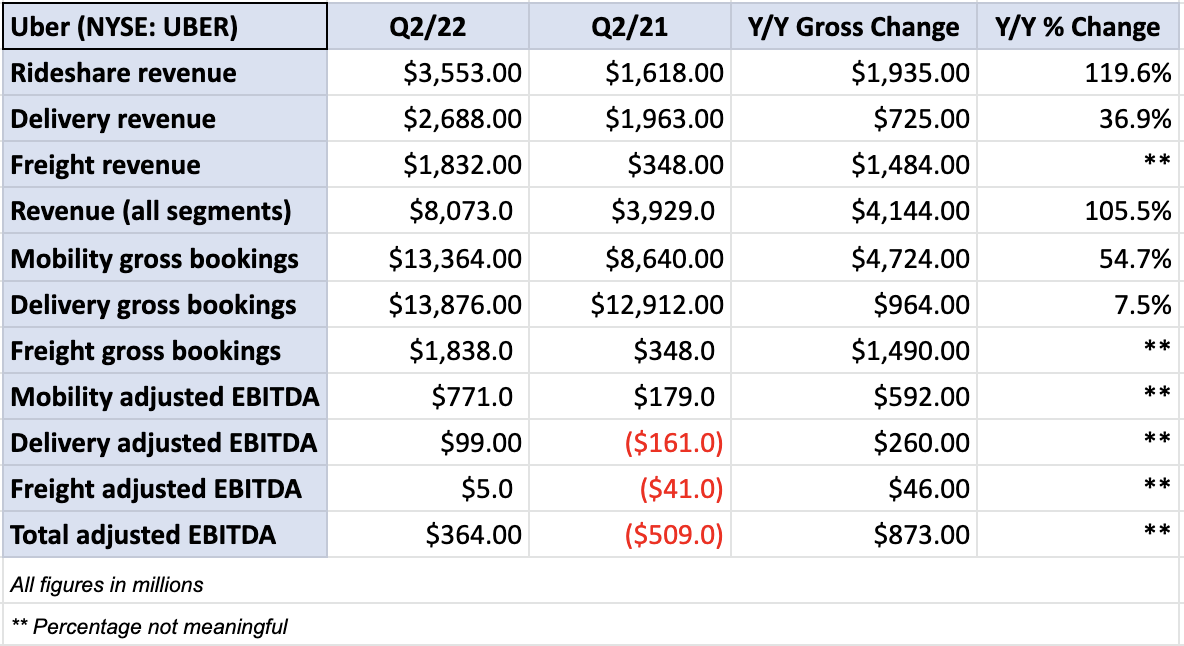

After Eats and all its delivery business guided Uber (NYSE: UBER) through the pandemic, ridesharing appears again in the driver’s seat. Due largely to expansion in its mobility sector, the corporation posted record second-quarter 2022 sales of $8.1 billion, up 33% from last year. Uber’s platform was used by 5 million drivers and 122 million customers, more than ever in Q2, which helped it make up for losses on its investments in Aurora, Grab, and Zomato. Another significant achievement was the company’s free cash flow, which reached $382 million and was positive for the first time in a quarter. Uber generated a profit from its operations rather than a loss.

Uber’s share loss per share was $1.33, which was less than the consensus estimate of 47 cents. Losses from investment in other ridesharing or food delivery services were $1.7 billion, although the company’s revenue exceeded analyst projections by $700 million. This contributed to adjusted earnings of $364 million, which exceeded Uber’s high-end projection for the quarter. Also, it represents a rise of about $873 million from the previous year. Gross bookings increased 33% yearly to a record $29.1 billion. The number of trips increased 24% yearly to 1.87 billion, 12% more than in 2019 before the epidemic. During the same period, drivers and couriers made $10.8 billion on the platform, an increase of 37% year over year and a 33% increase above gross bookings.

Customers having the option to place orders after hours may be the largest enhancement to the app’s grocery delivery service. Customers would be able to shop even if a store was closed and have the order delivered the next day at the time of their preference. Additionally, Uber expanded the scope of its order-tracking technology beyond the delivery path. Customers may watch each item scanned and bagged in the store in real time. Customers may now order items offered by weight and find replacements for out-of-stock products more easily, thanks to changes made to the platform.

India market continues to be a duopoly – Detailed comparison.

There have been developments like new SKUs and prices by restaurants on Zomato and Swiggy with quantity variation in the “barely visible” range due to the lack of uniformity (on grammage). Both aggregators have good self-control when it comes to discounts and shipping charges. The average “best” bargain discount during the current 60% off sale is Rs 100 (25% of AOV, Rs 75 at Swiggy). Depending on how long these discounts last, Zomato’s discount share will probably range between Rs 8 and 15 for each order. With a moderate degree of demand inelasticity, the average delivery price on Zomato grew significantly to Rs 33 per purchase (+22% v/s FY21, Rs 37 on Swiggy). There is room for an additional increase due to the Next 500’s lower delivery price (Rs 24 per order). In general, improving delivery (fees & costs) would be a major factor in increased contribution.

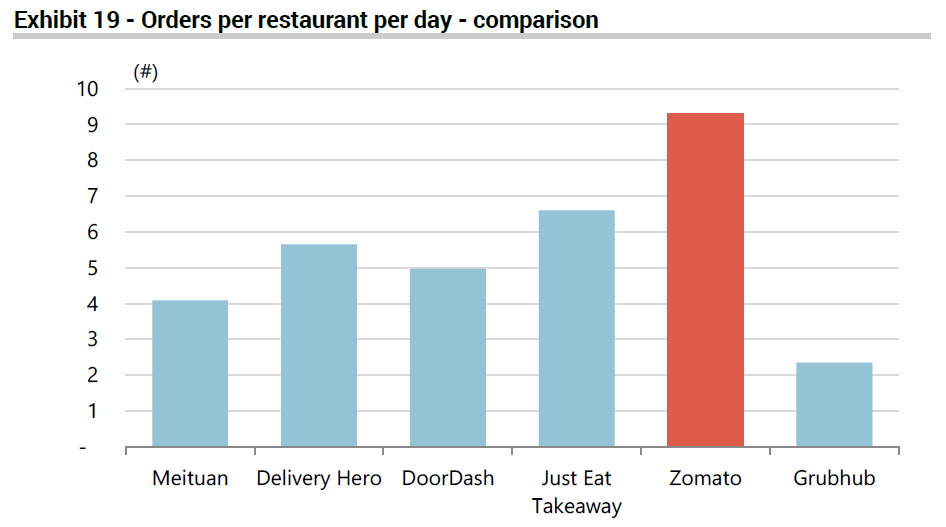

Zomato has one of the largest order volumes per restaurant per day compared to its regional and international competitors.

Despite having a US$65 billion market in absolute terms, India currently lacks a sufficient supply of restaurants that deliver food. Given the characteristics of the market, a sizable portion of suppliers are disorganized and offer inexpensive goods that are unsuitable for listing on the platform for meal delivery. Zomato has had a network of more than 140k active service restaurants as of the end Mar-20, which served an annual delivery capacity of over 400 million orders, demonstrating the restriction. In contrast, Meituan (the market leader in China) serves 10 billion orders annually and has 6.8 million eateries listed on the delivery platform. Even larger worldwide businesses than Zomato have a considerably larger selection of restaurants on their platforms. In fact, among six meal delivery tech platforms, Zomato has the largest number of daily orders per active delivery restaurant.

US delivery app stock: Doordash, Revenue sources (Existing Section)

The company earns its revenues from these four sources:

- Commissions: The company charges a service fee of around 20% to the restaurants for collaborating with them and for the delivery program. Restaurants are fine with paying these commissions as they can reach a wider audience base and have the delivery system at their disposal.

- Advertising: The company has monetized customer loyalty by helping the restaurants grow. Restaurant owners use the app to promote their business and reach out to customers about special discounts and offers.

- Delivery Charges: The charges have been quite minimal regarding DoorDash’s delivery fees range between $5-$8 per order.

- DashPass: This is a subscription model offered to its customers, which helps them save on delivery charges and service fees. It is priced at $9.99 monthly and helps the customers save about $4-$5 on each order. Customers with the pass do not have to pay for delivery service over $12. Hence a win-win for both.

In the case of Zomato, online food delivery in India is expanding quickly from a small basis. According to industry forecasts, growth will average 22% during 2025–2030 and 35% over 2020–25. At this rate, the online meal delivery market would expand from USD 4.2 billion in 2019 to USD 35 billion by 2030. Food delivery’s share of the restaurant industry is anticipated to rise from 6.5% in 2019 to 16.2% by 2030, a significant increase from the current penetration rates in more developed areas like the US (6%), China (15.6%), and South Asia (10.2%). Similar slowing tendencies are being observed in e-commerce as the customer base grows.

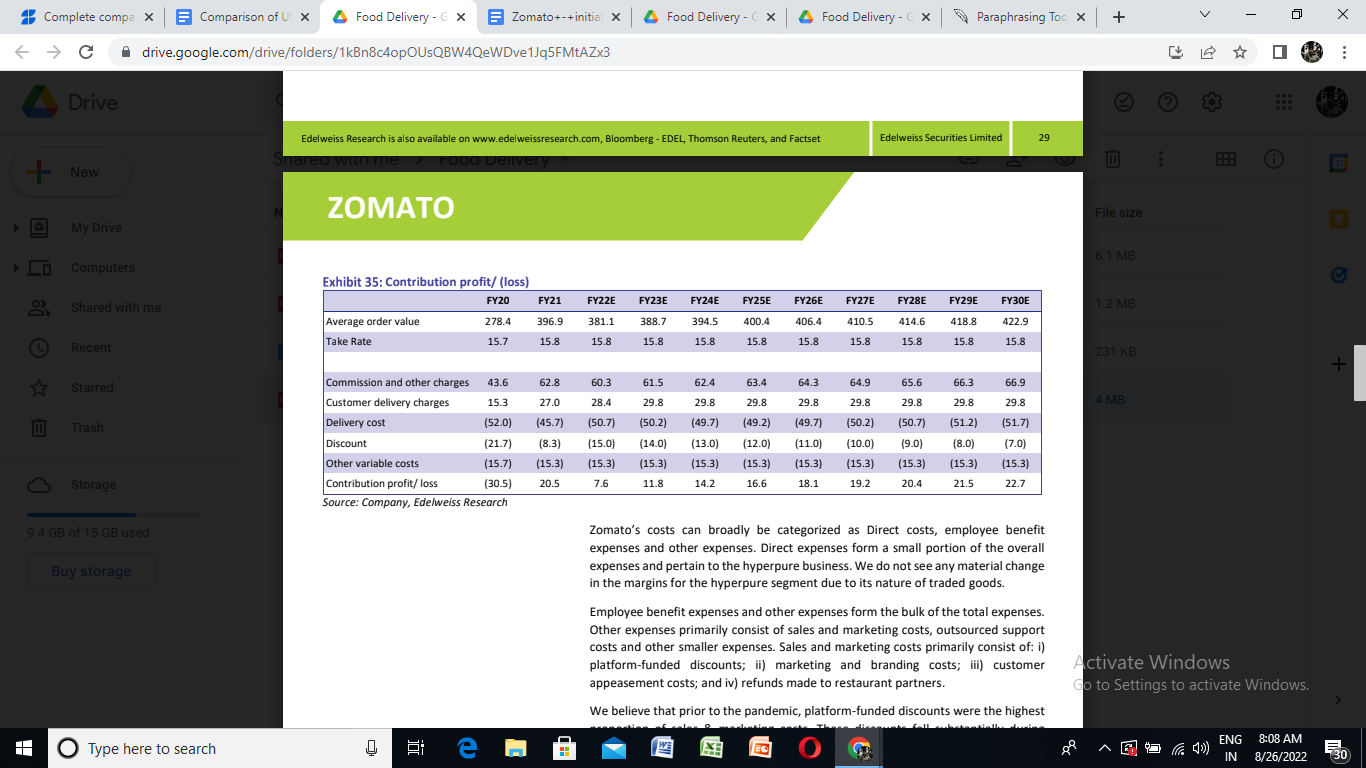

Contribution Profit/Loss for Zomato:

Take Rate for Zomato:

Key Takeaway

Compared to US enterprises, the companies in India have a significantly bigger targeted market share and space for expansion. The valuation is comparable to US delivery app stocks, though. Performance indicators for US stocks, such as AOV and EBITDA margins, are substantially better, whereas Indian businesses are losing more money. Read more on things to keep in mind while investing in US stocks before buying US food delivery app stocks.